FMW-Redaktion

Die Bank of Japan druckt Geld wie sonst niemand, der Staat verschuldet sich in obszönem Ausmaß – alles bekannt. Immer mehr zeigt sich, wie wenig diese Politik wirkt. Keinerlei Auswirkung bei der Inflation! Wie wir schon mehrmals schrieben: Bei einer kräftig schrumpfenden Bevölkerung und einer hoch-produktiven Industrie mit dementsprechendem Preisdruck wird es schwer selbst mit solchen Maßnahmen die Inflation aus dem Hut zu zaubern! Sehr gut visualisiert ist diese desaströse Entwicklung in diesem Vergleich. Die Bilanz der Bank of Japan steigt immer weiter, während die Inflation immer weiter abrutscht.

Bank of #Japan fails to stimulate #inflation. Japan stuck in #deflation for an 8th mth despite totally mad balance sheet expansion. pic.twitter.com/r3ny9Yd6To

— Holger Zschaepitz (@Schuldensuehner) November 25, 2016

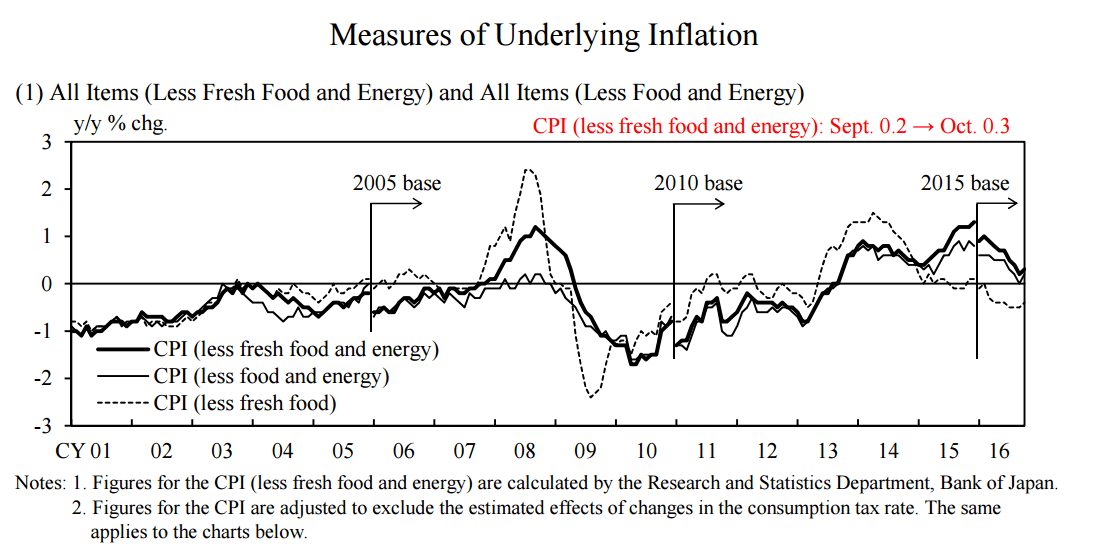

Selbst ohne Energie knappst die Inflation in Japan an der Null-Marke, wie diese heute veröffentlichte Grafik der Bank of Japan zeigt.

Grafik: Bank of Japan

Eine Frage von uns Kleingläubigen: Warum haben irgendwie alle großen Notenbanken exakt das selbe Ziel, die Inflation auf genau 2% bringen? Ist das die heilige Marke aller Ökonomen? Naja…

Wie auch immer, die Bank of Japan hat ebenfalls das 2%-Ziel, liegt derzeit aber tot um die 0% herum. Während die EZB meint grob geschätzt Ende 2017 in diese Richtung zu gehen, rechnet die Bank of Japan mit „irgendwann im Jahr 2018“. Stand heute ist das illusorisch. Die Aussagen, die Notenbank-Präsident Kuroda erst am Dienstag offiziell machte, zeigen das einmal mehr. Wie seine Kollegen in europäischen Notenbanken glaubt auch er alleine mit seiner „Geldpolitik“ alles bis ins Kleinste steuern zu können. Zitat:

–

–

Japan’s economy has continued its moderate recovery trend, although exports and

production have been sluggish due mainly to the effects of the slowdown in emerging

economies. With regard to the outlook, it is likely to continue growing at a pace above its

potential through the projection period — that is, through fiscal 2018 — with a virtuous cycle

from income to spending being maintained in both the corporate and household sectors, on

the back of highly accommodative financial conditions and the effects of the government’s

large-scale stimulus measures, as well as the recovery in overseas economies.

On the price front, the year-on-year rate of change in the consumer price index (CPI, all

items less fresh food) has been slightly negative due to the effects of the decline in energy

prices. As for the outlook, it is likely to be slightly negative or about 0 percent for the time

being, and as the aggregate supply and demand balance (the output gap) improves and

medium- to long-term inflation expectations rise, it is expected to increase toward 2 percent

— the price stability target — in the second half of the projection period. The timing of the

year-on-year rate of change in the CPI reaching around 2 percent will likely be at the end of

the projection period — that is, around fiscal 2018. Thus, the momentum toward achieving the price stability target of 2 percent seems to be maintained. However, it is somewhat

weaker than the previous outlook made in the July Outlook Report, and thus developments

in prices warrant careful attention going forward.

II. Conduct of Monetary Policy

At the September 2016 MPM, the Bank conducted a comprehensive assessment of the

developments in economic activity and prices, as well as of the policy effects since the

introduction of quantitative and qualitative monetary easing (QQE). Based on its findings,

with a view to achieving the price stability target of 2 percent at the earliest possible time,

the Bank introduced „QQE with Yield Curve Control,“ which is a new framework for

strengthening monetary easing. This framework consists of two major components.

Kommentare lesen und schreiben, hier klicken