FMW-Redaktion

Warum hat Donald Trump so einen Zulauf? Könnte das hier ein Teil der Erklärung sein? Für einen großen Teil der US-Bevölkerung steigen schon seit 10-20 Jahren die Löhne nicht mehr. Selbst bei minimaler Inflation erlebt ein Großteil der Bevölkerung sogar eher Einkommensverluste. Wie soll man da seinen Lebensstandard halten? Richtig, man lebt auf Kredit. Immer mehr Kreditlast zu schultern bei gleichzeitig immer weniger Realeinkommen, da will man irgendwann jemanden, der einem Besserung verspricht? Ob die tatsächlich eintritt, ist eine andere Frage, aber das strukturelle Problem wächst immer weiter an, egal ob Bush oder Obama gerade regiert.

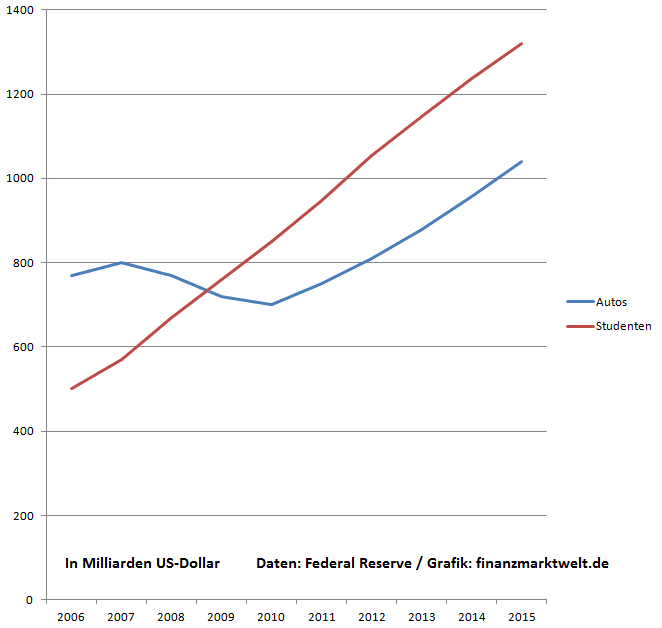

Die US-Notenbank Federal Reserve weist die Posten Autokredite und Studentenkredite als Einzelposten aus, so dass ihre Entwicklung nachvollziehbar ist. Die Fed-Filale St. Louis beschäftigt sich viel mit Statistiken und hat jetzt neueste Zahlen veröffentlicht. Seit 2012 würden in den USA 90% des Wachstums bei Krediten aus Auto- und Studentenkrediten resultieren, so die „St. Louis Fed“.

In der Grafik oben ist die Verschuldung bei Auto- und Studentenkrediten im Schnitt pro Schuldner in tausend Dollar zu sehen. Sie nimmt kontinuierlich zu – bei Studentenkrediten in 12 Jahren von 16.000 auf 25.000 Dollar pro Kopf, bei Autokrediten fiel sie von 2003 bis 20011 von 12.000 auf unter 11.000, jetzt ist man zurück auf dem alten Hoch und steigt weiter an. Zitat:

Borrowing for Higher Education and Automobiles Are Driving Debt Rebound

Consumers across the country are borrowing more to finance car purchases and pursue higher education. For both the nation and the District, student and auto loans combine for around 90 percent of debt growth since the fourth quarter of 2012. In Figure 2, the remarkable growth is reflected by the average amount of auto and student debt held by borrowers.2 Average auto debt grew at a similar rate to student loans since the close of 2010. However, unlike auto loans, the recession did little to slow the growth of student loan balances. Since 2003, the average student loan balance has increased by more than 58 percent. Some reports argue that part of the slow recovery is due to recent graduates paying down student debt rather than buying houses and other goods.3 Figure 3 breaks down the growth in both student debt and auto debt by age groups and highlights the groups generating the majority of the economic activity. The vast majority of new student loan debt is concentrated in younger age groups. Coupled with consistently rising average balances, this heavy concentration of new debt among the young supports the theory that these borrowers will experience headwinds in the form of a longer deleveraging period before other spending or saving decisions may be financially sound. In contrast, much of the new auto debt is concentrated in the older age groups. This is especially true for the District, where 61 percent of new auto debt was accumulated by individuals age 56 and above.

Consumers across the country are borrowing more to buy cars and go to school https://t.co/mkKAoVya2o pic.twitter.com/DxMiHo7kki

— St. Louis Fed (@stlouisfed) March 3, 2016

Student and auto loans combine for about 90 percent of debt growth since 2012:Q4 https://t.co/ijZ31Y9xgq pic.twitter.com/PM5aiY2Hw3

— St. Louis Fed (@stlouisfed) March 2, 2016

Auto debt is rising, driven largely by older borrowers https://t.co/gZnA7WLEDy pic.twitter.com/pUsqtsZMoA

— St. Louis Fed (@stlouisfed) March 3, 2016

Kommentare lesen und schreiben, hier klicken