FMW-Redaktion

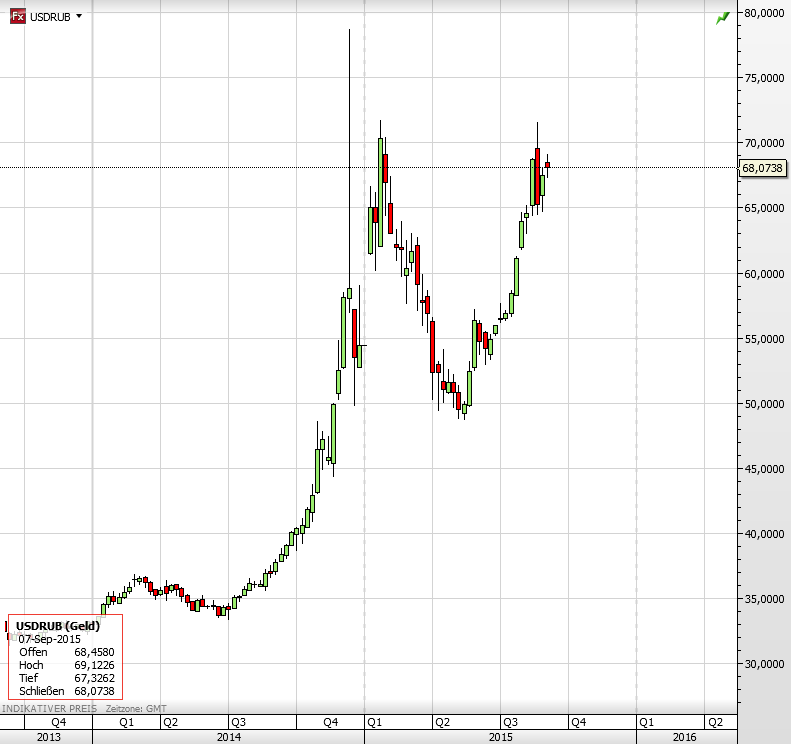

Die russische Zentralbank hat auf ihrer heutigen Sitzung den Leitzins unverändert bei 11% belassen. Sie sieht Inflationsrisiken für Russland inmitten einer potenziell schwächelnden Wirtschaft – erstaunlich! Es geht wohl um das Abwägen: Senkt man den Leitzins, hilft man tendenziell der Inlandswirtschaft – dadurch schwächt man den Rubel gegenüber Fremdwährungen aber noch weiter. Der ist aber jetzt schon extrem abgewertet, und USDRUB würde wohl das 70er-Level nachhaltig nach oben überschreiten.

Hier der wichtigste Teil des Statements der Central Bank of Russia:

„On 11 September 2015, the Bank of Russia Board of Directors decided to maintain the key rate at 11.0 percent per annum, due to the higher inflation risks amid persistent risks of considerable economy cooling. August saw a serious deterioration in foreign economic conditions. Inflation and inflation expectations were showing a clear upward trend, impacted by the exchange rate dynamics. The depreciated ruble will continue to put pressure on prices in the next few months. However, the relatively tough monetary conditions and slack domestic demand will drag down annual inflation. The annual consumer price growth rate in September 2016 is estimated to be about 7%, reaching 4% in 2017, which will be facilitated by the current monetary policy. The Bank of Russia will subsequently revise its key rate based on the balance between inflation risks and the risks of economy cooling.

Annual inflation rose from 15.6% in July to 15.8% in August. As of 7 September 2015, consumer price growth remained unchanged, according to the Bank of Russia’s estimates. The ruble’s depreciation caused prices for a wide range of goods and services to accelerate, which was the reason for elevated inflation expectations, along with the July indexation of utility tariffs. The ruble’s decline observed in July-August will continue to put pressure on inflation in the next few months. The moderately tough monetary policy and weaker consumer demand on the back of significant contraction in real income are projected to hamper consumer price growth.“

–

–

Kommentare lesen und schreiben, hier klicken