FMW-Redaktion

Gibt es da eine Zeitenwende? Anscheinend ist Russlands Notenbankpräsidentin Elvira Nabiullina jetzt darauf aus ausländische Investoren ins Land zu locken und die Wirtschaft anzukurbeln. Nicht nur, dass letzten Freitag der russische Leitzins von 11% auf 10,5% abgesenkt wurde. Damit liegt der Leitzins jetzt genau da, wo er vor der dramatischen Anhebung auf 17% Ende 2014 war um einen totalen Kollaps des Rubel zu vermeiden. Nabiullina stellt aktuell öffentlichkeitswirksam beim Wirtschafts-TV Nr.1 in den USA „CNBC“ weitere Zinssenkungen in Aussicht. Auch sehe man verbesserte Erwartungen ausländischer Investoren für die russische Wirtschaft, für Investitionen in Russland und die hiesigen Aktien. Aktuell sei die Zinssenkung möglich gewesen wg. der im dritten Monat nacheinander konstant gebliebenen Inflation bei 7,3%. Die Luft für weitere Zinssenkungen sei da, und natürlich gehe es nicht um einen Abwertungskrieg, Zitat:

„The potential for a further reduction of interest rates is there, because if you take a look at our nominal and real rates, they are fairly high right now,“ Nabiullina told CNBC. She added that she was not worried by the possibility of an international „currency war,“ despite concerns raised by economists and politicians over the last few years that countries were competing to debase their currencies, partly in a bid to make exports more competitive. „I see very little risk of any serious currency wars breaking out. I think that many central banks and financial authorities understand that any long-term attempt to compete through an artificial depreciation of their currency (would not) be very effective in the long term,“ she said.

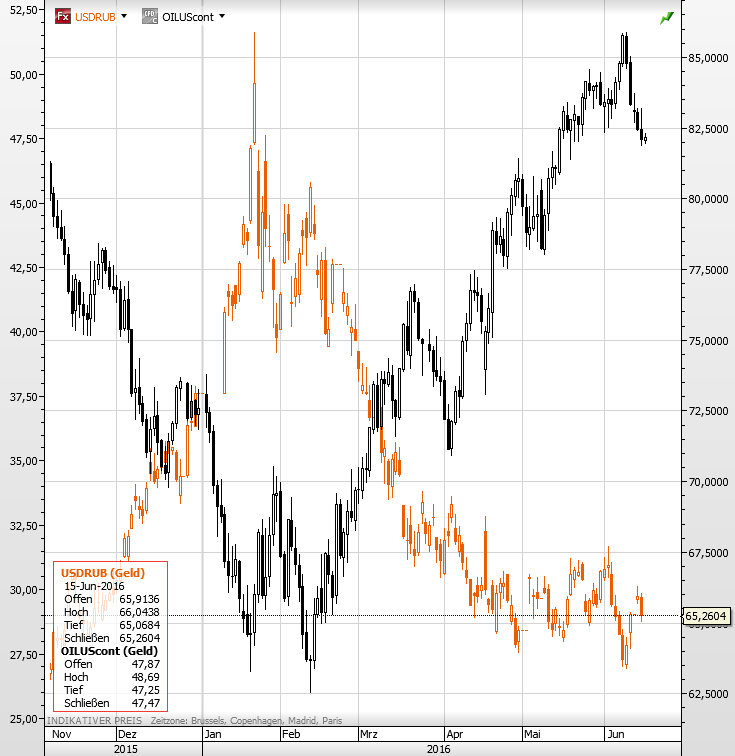

Die Hinwendung zur Ankurbelung der Wirtschaft, das kann man schon als eine Zeitenwende der Notenbank ansehen. Offiziell geht es nur um die Inflation, die im Griff ist, aber Nabiullina´s umfassende Kommentare zu ausländischen Investitionen sollen doch wohl heißen: Wir senken die Zinsen, kommt zu uns. Ein Problem hat die russische Notenbank da leider: Jetzt wo man unausgesprochen versucht die Wirtschaft mit einem schwächeren Rubel anzkurbeln, unterstützt der seit Monaten kräftig gestiegene Ölpreis einen Rubel, der nicht fallen will. Der US-Dollar fällt hingegen seit Monaten eher gegen den Rubel (orange).

Gibt es eine Zeitenwende in Russland? Mehrere weitere Zinsschritte zum „Auflockern“?

USDRUB (orange) vs Öl (schwarz) seit Ende 2015.

Offiziell ist viel von Inflation die Rede. Die sei unter Kontrolle, daher die Zinssenkung und die Aussicht auf weitere Schritte. Hier der Originaltext der russischen Zentralbank von der Zinssenkung letzten Freitag:

–

–

In making its key rate decision, the Bank of Russia Board of Directors has proceeded from the following factors.

First. There is more confidence in steadily positive trends in the inflation dynamics. Consumer prices grew less than predicted. The annual inflation has stabilised at 7.3% and the annualised monthly inflation, seasonally adjusted, is about 5%. Economic activity indicators improve along with ongoing low consumer demand and a high rate of savings without creating upward pressure on consumer prices. Inflation expectations of households and businesses continue to decrease. The situation in the global commodity markets was more favourable than expected and contributed to the inflation slowdown through the ruble exchange rate and food price movements (these factors’ influence is temporary and is subject to decrease, which is considered in the inflation forecast). The administered prices and tariffs will be adjusted in July in compliance with the stated plans, but to a lesser extent than a year ago. Consumer price growth rates will keep on going down further, primarily influenced by the demand-side restraints. The Bank of Russia marked down its inflation forecast for the end of 2016, to 5-6%. Considering the decision just made and retaining the current monetary policy stance, the annual inflation will be less than 5% in May 2017 to reach the 4% target in late 2017.

Second. Positive trends in the economy are not accompanied by a higher inflationary pressure. The figures of the GDP dynamics in 2016 Q1 and macroeconomic indicators for April confirm greater sustainability of the Russian economy to oil price fluctuations. Import substitution and non-commodity exports continue to expand and additional growth areas in manufacturing are taking shape. However, the changes in economic dynamics vary across the industries and regions. Investments continue to show a downward trend and a wide range of industries experience stagnation, including those that have traditionally been the sources of growth for the Russian economy. Yet positive shifts in the economy anticipate the beginning of its growth recovery. Quarterly GDP growth is expected no later than 2016 H2. The forecast predicts a GDP increase of 1.3% in 2017 and annual growth rate for output of goods and services remaining low in the following years. The forecast is based on a fairly conservative estimate of the annual average oil price, which is approximately $40 per barrel over the three-year horizon.

Third. Monetary conditions will still be moderately tight, despite a slight easing due to the lowering banking sector liquidity deficit. Real interest rates in the economy (adjusted for inflation expectations) will remain at the level that encourages savings and allows for demand for loans that does not cause an increase in inflationary pressure. In order to ensure operational control over the level and structure of market interest rates in the context of the emerging transition to the banking sector liquidity surplus, the Bank of Russia is ready to take a set of measures designed to mop up liquidity.

Fourth. The risks that inflation will not reach the target of 4% in 2017 declined, but still remain at a heightened level. This primarily stems from inflation expectation inertness, the lack of mid-term budget consolidation strategy and the uncertainty in the parameters of future indexation of wages and pensions. Volatility in the global commodity and financial markets also might have a negative impact on the exchange rate and inflation expectations. The materialisation of these risks might cause a slowdown in the inflation reduction.

–

–

Kommentare lesen und schreiben, hier klicken