FMW-Redaktion

Die russische Zentralbank belässt den Leitzins unverändert bei 11%, schon das fünfte Meeting in Folge. Die Kernaussage der Zentralbankchefin Elvira Nabiullina lautet: Wir achten auf die Inflation, die darf nicht weiter angeheizt werden, deswegen können wir jetzt die Zinsen nicht senken. Dabei würde sich die Wirtschaft selbst wohl sehr über deutlich tiefere Zinssätze freuen – ein Dilemma für Russland!

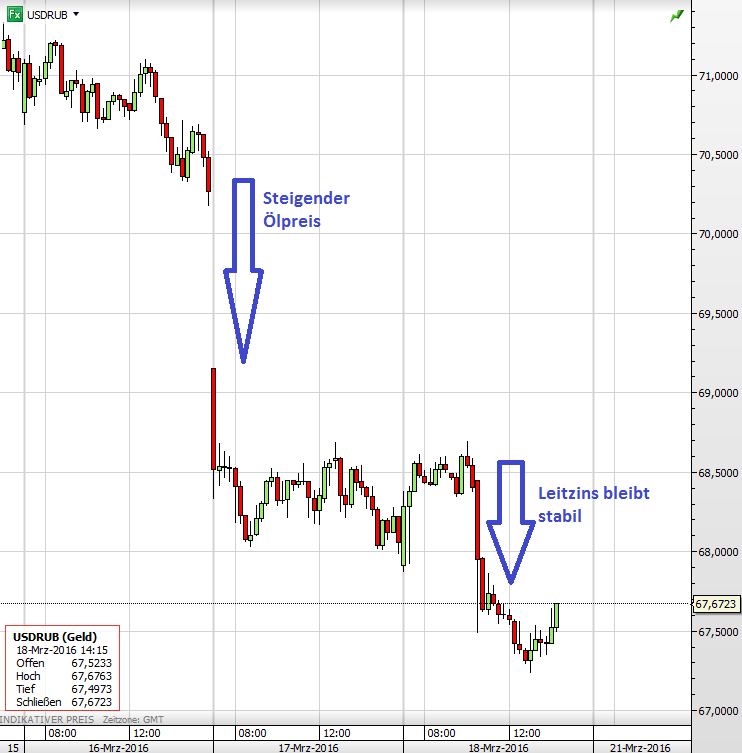

USDRUB kurzfristig.

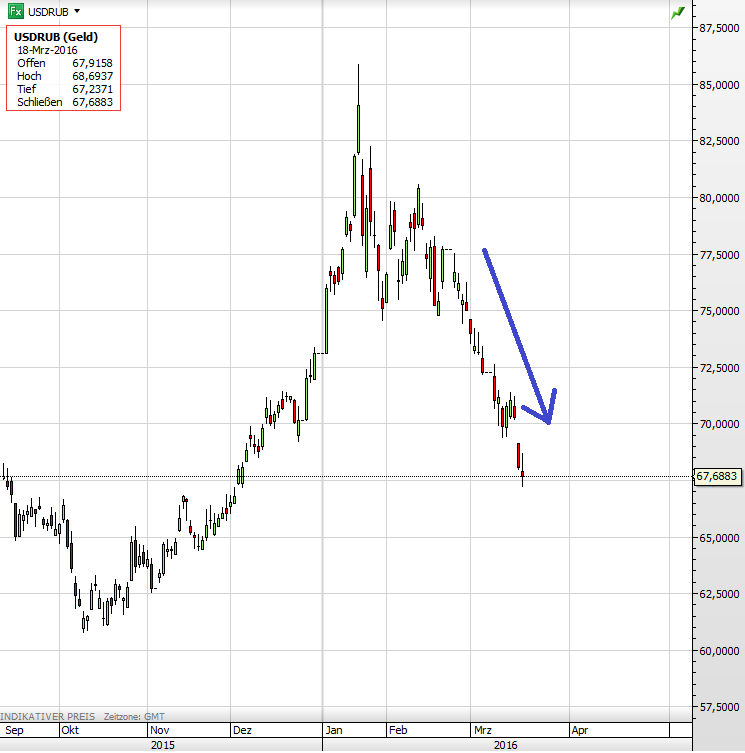

USDRUB seit September 2015.

Keine fallenden Zinsen bedeuten keine schwächere Währung. Dementsprechend wertet der Rubel heute weiter auf. Im Umkehrschluss stellt sich dies in einem fallenden Dollar gegenüber dem Rubel dar. USDRUB ist von Mittwoch auf Donnerstag schon kräftig gefallen im Zuge des massiven Ölpreisanstiegs zum selben Zeitpunkt. Jetzt legt der Rubel durch den stabilen Leitzins nach und wertet noch ein Stück weiter auf. Wie der Langfristchart zeigt, zeigen steigende Ölpreise + ein stabiler Leitzins auf Sicht mehrerer Wochen eine kräftige Wirkung pro Rubel. USDRUB fiel seit Mitte Februar von 77 auf 67.

Und die Äußerungen von Elvira Nabiullina lassen auch keinen Zweifel an einer weiter stabilen Politik. Zitat (auszugsweise):

We must ensure a steady path of reducing inflation to our target of 4% by end-2017. We are perfectly sure that only low inflation is a guarantee of stability and low interest rates in the economy. In order to keep interest rates steady and low, we should first ensure sustainably low growth rates in consumer prices and a decrease in high inflation expectations. Then, proceeding from this, we will have stable and low interest rates. This requires a consistent and gradual interest-rate policy of the central bank. That is why the Bank of Russia may pursue a moderately tight monetary policy for a longer period of time, then assumed earlier, to achieve the inflation target.

Inflation

The recent data of 14 March suggest that annual inflation is 7.9%. In the February to March period, it was decreasing somewhat quicker than we expected in January. We expected it to be at 8%-9% for the end of Q1. This takes me back to the 9% reading for March 2016 we forecast a year ago. Average daily price increment in March was at this year’s low. This performance is explained by several reasons.

Inflation risks

Importantly still, inflation risks, that is, the risks that inflation may cease to decline or decline slower on the way to the target, remain high. The core risk sources are as follows.

– First. Oil market instabilityI have covered this.

– Second. The risk that elevated inflation expectations would remain. They are currently resuming to decline, but they remain high. It is crucial that the trend towards reduced expectations remains and becomes more sustainable. In the first place, this must be prompted by slowing actual inflation; however, confidence in the Bank of Russia-implemented monetary policy is here of crucial importance, too. We are concerned about elevated inflation expectations expressed by professional analysts and economists.

– Third. Here we are faced with several uncertainties surrounding budget configuration, in particular, the prospects for extra indexation of pensions and wages. This risk source may be the most important. A balanced fiscal policy is essential for the economy. Given the change in external conditions, a ceiling on deficit and budget spending growth must be set down. Here we need a mid-term clear strategy to reach balanced budget so that all economic agents are fully knowledgeable about budget deficit over three years’ horizon and about the sources of its funding. A consistent and responsible policy is a precondition for stable economic development, as well as key prerequisite for lower inflation and financial stability risks. Analysis shows that, all other things being equal, more conservative fiscal policy allows for softer monetary policy, and vice versa.

– Fourth. The prospects for a turnaround in the global food prices. This would also have negative influence on annual and monthly inflation in Russia. As is usually the case for this time of the year, there remains uncertainty surrounding Russian crops, which would potentially have influence on 2016 prices.

We recognise all these risks as we make our key rate decisions.

Kommentare lesen und schreiben, hier klicken

Lächerlich was die Nabiulina macht, aber brav ist die… Russische zentral Bank ist eine Tochtergesellschaft der FED, gibt’s noch Fragen….???